A Summary of the 2018 Investment Market woes and the outlook for 2019 and how we see portfolios to be best positioned – at the best price for advice … A rear view review of 2018 (the easy bit!)

A year of messy politics and economic policy change broke the calm of investment markets in 2018. 2017 had been a year of very low investment volatility….

The investment markets in 2018 started the year strongly, disregarding the negatives of the political scene, focusing instead on the tax cuts in the US, fueling optimism for growth, supported by near ‘full employment’ in the USA, with the UK looking well positioned also.

By way of an example that most UK investors understand;

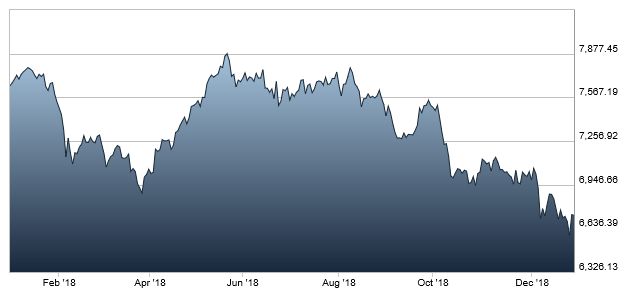

The main UK index (FTSE 100) started 2018 @ 7648.10, following strong gains in December 2017, where a Santa Rally was certainly in play…

Mid January saw the first signs of realism and concern, where investment market traders took profits and the markets became more ‘risk off’ for the first time in a year or so… the thinking was created by a change in economic policy and an expectation of interest rates increasing quickly on both sides of the Atlantic Ocean.

By March 22nd 2018, the FTSE 100 closed at 7121.90. ‘Risk off’ in the UK and USA lasted only briefly, as the FTSE 100 had ended the trading day at 7859.20 on 20th May 2018 (An all time close of trading high). However, the Emerging Markets were suffering at the hands of the US$, along with trade war concerns.

The US v China stand off in relation to trade started to hit Global markets mid year, with volatility truly returning to markets and investors’ thinking.

A graph of the last 2 months of the FTSE 100 looks more akin to a cliff edge when viewed over a 12 month period.

FTSE 100

The FTSE 100 ended the year at 6728.13 so ending the ‘bull’ investment market that has run for the longest period in investment history.

Investor champion described 2018 as ‘bleak and bruising’ year for investors, producing the worst year-end finish to investment markets since 2008.

In other words; the investment markets have become ‘Risk off’ – with traders and investors becoming ‘jumpy’ and selling at the reading of a ‘tweet’, rather than considering the fundamental economic environment

A rear view review

The tail end of 2018, leading into 2019, is seen as ‘far from a normal market’

A look back at the hottest business stories of 2018.

I append a link to a BBC news article for a fuller detailed read of the ‘stories’ that happened in 2018 : https://www.bbc.co.uk/news/business-46481167

January 2018

A grim start to the year saw one of the biggest providers of public services support in trouble – Carillion. Leading to collapse.

February 2018

Saw the investment markets take a ‘reality check’ following a year of next to no volatility.

March 2018

The big story was the ‘Beast from the East’ and the knock on to the impact.

April 2018

The major story in the UK was that Sainsbury’s and Asda were in merger talks.

Brexit starts become a focus and a reality to investment markets.

May 2018

Homebase was sold for £1.

June 2018

A Heatwave.

The effects on produce became apparent and so to climate change impact. Climate change became prominent in the media.

July 2018

The Heatwave continued …. more woes for growing producers/farmers.

Johnson & Johnson were ordered to pay 22 women £3.6bn due to talc product causing ovarian cancer.

August 2018

House of Frazer in trouble – ultimately purchased by Newcastle United’s owner, Mike Ashley, and his Sports Direct group.

September 2018

Trump and Tariffs are front and central.

Eton Musk’s tweet loses his position as Tesla Chairman.

October 2018

Investment market nerves take hold, following Trade Wars and economic policy change. Volatility returns with a vengeance….

November 2018

Carlos Ghosn, Head of Nissan-Renault-Mitsubishi partnership, was arrested in relation to financial misconduct.

Brexit again – becoming an everyday story …. focus becomes the negative of a ‘no deal’ Brexit.

Trade Wars are also a constant feature of economic news.

December 2018

Stock Market woes – amidst a backdrop of political mess in the UK and the Trump Tweets continue …..

So – what is happening with the Investment Markets?

Volatility over the last 3 months or so has increased, meaning that market makers have become concerned about news flow, dominated by Geo Politics and National Political issues, along with Economic policy change, trade concerns and, of course, Trump … and his tweeting…. On the run up to 2018 year end the investment markets had little good news to ‘Trump’ about!

Employment numbers and economic data remain on or above trend, where mid year the data was above trend, slowing somewhat maybe, but seen by many economists as remaining strong currently.

In an article on Bloomberg surveillance on Friday 28th commentators Kit Juncker – Global Fixed Income strategist at Société Generali and Diana Amoa, Senior Portfolio Manager at JPM Asset Management, agreed that there is ‘value in equity markets’ –https://www.bloomberg.com/news/videos/2018-12-28/-bloomberg-surveillance-full-show-12-28-2018-video

Kit Juncker stated on the programme that even the biggest of ‘bears’ did not expect the ‘sell off/correction’ to be as big as it has turned into. The FTSE 100 index (Peak to Trough) over the 2018 year would have reduced in value by 15% or so… with Banks and Autos suffering greater pain.

Therefore, those holding a main market FTSE 100 tracker suffered badly over the year.

Most leading economists are not forecasting a ‘deep Global recession’ so it may be that the market makers have become a little too pessimistic, following a period of being a little too optimistic….?

Many investment analysts ‘think’ that the economic cycle is now beyond the ‘peak in the growth cycle’ but we are some way off contraction.

Investment markets have suffered considerable volatility in the final week of 2018, on the back of little or no economic news… Trump’s tweet in relation to the US Federal Reserve and the “interpreted” potential sacking of Fed Chairman Jerome Powell created a big concern to the markets, at a time when trading volumes were smaller than other times of the year.

One would have thought that political interference in Monetary Policy would be the domain of Turkey; not so in 2018, it was Trump’s USA.

Politics of a Mad House spring to mind!

‘All options’ are communicated on Social Media in this current space……!

The sooner that the investments markets are evaluated on the ‘fundamentals’ of the economy and the macro/micro picture of the asset held, the better, so Mad House politics can be seen as an error of the political programme and time….

Slower Global Growth in 2019?

The US remains strong, according to the data, although the negatives sometimes deliver a self-fulfilling prophecy.

The ‘Trade War’ between the US and China remains concerning, although at times an accord seems to be achieved. A number of commentators have suggested that the USA and China are likely to ‘agree’ a way forward, with a compromise on Trade. (As this note is written, Trump is releasing information based around the Trade talks making ‘big progress’), although it’s likely that trade disputes are not easily fixed.

China is slowing, with the borrowing China has created failing to deliver the boost in growth expected. This is likely to have been impacted by the ‘noisy backdrop’, so in a more normal political environment the borrowing may have boosted growth?

China is now focusing on the domestic consumers and high end manufacturing, rather than infrastructure.

Kit Juncker of Société Generali confirmed on Bloomberg that ‘no forward guidance on monetary policy comes from Beijing’ – he gets guidance from the US Federal Reserve (Fed), European Central Bank (ECB) and the Bank of England (BoE) and Bank of Japan (BoJ).

Brexit

‘All options remain on the Table’ – it seems!

The third week of January is likely to produce a little more transparency, following the Chamber in the House of Commons vote on PM May’s proposed ‘deal’ likely to take place.

There is likely to be further ‘Brinksmanship’ between parties and the EU so the outcome for now is certainly unclear, which investment markets dislike. (We will continue to provide our clients with updates in this area as developments unfold).

https://www.bestpricefs.co.uk/blog/politics-drive-investment-markets-lower/

Emerging Market respite

The Dollar holds the key to the position with the Emerging Markets sector. Some leading commentators suggest a gradual weakening of the US Dollar over the course of 2019 – which would be kinder to the EM sector.

Holding quality is key in this sector – and taking a long term view.

Dreadful December 2018 – has now past… bring on 2019

Levels of support may now be a little more resilient, with traders willing to hold risk assets, rather than dumping them promptly on the first sound of negative noise – in this negative noise environment.

So has all of the Bad news been priced in?

Unlikely, but falls may be shallower, based upon an expectation of asset price value, unless the ‘background’ to the economic environment changes….

Mid Year investor FOMO in 2018

The mid year ‘Fear of Missing Out’ has developed into a wry smile for those sitting on their hands. But remember, investing is a marathon not a 100m sprint.

Investors must ‘look through’ short termism and focus on their financial objective (Goal) – such as obtaining a specific retirement date and income – provided by hard work and making good long term investment decisions to meet their needs.

In Conclusion – the best way to invest and hold assets in 2019; at the best price

We, along with most views, are generally sanguine in relation to the noise surrounding the investment markets, trusting in the diverse asset allocation and quality of the asset management funds that we recommend to our clients, for medium to long term delivery of inflation beating returns. Of course there will be bumps in the road, sometimes deep bumps, but it’s important for investors to focus on their initial investment objective..

A range of Best of Breed, diversified portfolio of assets, measured against peers, using performance measurement tools and detailed Due Diligence of the assets in which our risk adjusted funds are constructed and recommended has delivered outperformance, although when markets fall, of course, risk models reduce in value also, our risk models are outperforming well in relative terms and remain on the “efficient frontier,” along the risk model scale, therefore meeting the investment brief and investment objective. It’s never pleasing when investment markets take a tumble but investing is never guaranteed and short term views should not be the domain of investors. It is always imperative to ‘get under the bonnet’ of the investment vehicle in order to ensure that the combination of the parts drive the ‘investment vehicle’ in a way that is suitable to the investors’ needs, considering ‘Risk’ as the focus to blending assets, picking funds, like throwing darts at a dart board is a certain way of producing ‘Risky and unsuitable investment outcomes’.

Investors must always be reminded that ‘Investing’ is not ‘Trading’ which is akin to gambling.

The recent falls in the Stock Markets have reduced Price Earnings (P/E’s) to around 11 – which is well below historical averages, which is likely to be the basis of commentators and analysts’ views that there is ‘value in equity markets’. Investment markets do not like uncertainty and the unknown (there is a contradiction here as the future is always ‘uncertain and unknown’!), which is why the current political backdrop has created such a ‘risk off’ investment market at the tail end of 2018.

Political Risk – we must expect politics to drive investment markets – certainly current at the start of 2019.

Making political and economic predictions is futile at the best of times and often renders the ‘crystal ball’ forecaster looking a little silly; so it’s best in our view to remain focused on investment objective and when the ‘facts change’ provide information and advise our clients accordingly.

Of course, it’s essential for investors to inform us if their objectives (goals) change, so we can collectively plan accordingly.

Best Price FS Risk Model Performance

Our asset allocation and performance data has delivered strongly over many years.

We deliver updates to our investment clients each quarter – so the ‘added value’ can be truly appreciated. You may wish to read a recent blog in respect to the use and diversity of funds used in our risk models.

If you would like to start a meaningful conversation about investing or reviewing your general financial planning and obtaining the best price for your financial services needs, simply get in touch.

Guarantees

We cannot guarantee investment outcomes and performance – no business, market commentator or individual can.

What we can guarantee is our focus and service and promise to offer financial consumers value for money, while buying and investing in leading financial products, without product bias or ‘shoe horning’ our clients into products that we own, therefore creating a commercial bias, potentially leading to a conflict of interest.

Always remember, we are independent advisers so are able to access the best quality products from the wide investment universe.

We are so confident in our advice track record and costs structure for advice that we ‘promise’, guarantee even to beat the published costs of any other advice service – relative to a comparable service in relation to advice provided on Investments, Pensions and Insurance. (This applies to electronic engagement and a suitability recommendation in order to be time effective and therefore cost efficient).

Our non-advised product purchase offerings speak for themselves. Check out our website, https://www.bestpricefs.co.uk. We provide products at the lowest margins possible- so if you can improve on the terms ‘like for like’ we will work for nothing if required in order to deliver to our consumer… (This is very unlikely, impossible even, that being said!).

Mission Statement

Our vision is to be a ‘one stop financial shop’ for our clients and consumers in 2019, so feel free to challenge us, we are committed to you, our client, and the national financial consumer, for their financial products and services.

Warmest Regards and Best Wishes for 2019.

Best Price FS Team