How to become your own ‘Master of the Coin’ – to ‘coin’ a Game of Thrones title and ensure investment decision provide a “safe investment environment” – delivering suitable outcomes – meeting investors’ needs and objectives.

Independent Financial Advice – Producing Quality Consumer Investment Outcomes….

The process, risks, potential outcomes and solutions …. A “must” read!

As Warren Buffet famously stated “Price is what you pay, value is what you get”. This statement applies to services, stocks and funds and most other aspects of life in our view, as discerning consumers…!

Warren Buffett also famously quoted “Someone is sitting the shade today because someone planted a tree a long time ago!”. Financial Planning requires time, the earlier the process is commenced the longer the ‘plan’ has to provide ‘cover’ and grow…… Plan wisely, early in life if possible, extracting value for money with all you purchase (products and services).

A very wise investment sage stated “buying pointless clutter is a waste of time and money – buy things you need and invest the rest – in excess of your contingency budget”…..

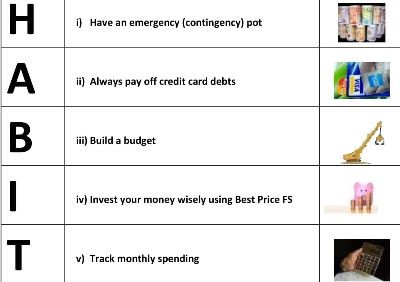

5 Financial Habits to live by:

Independent Financial Advice Service and product purchase offering

(Best Price FS value added process and journey)

We are often askeded by potential investors to explain the “journey and added value” outcome of engagement with a quality independent financial adviser – clarifying the benefits of financial regulation as opposed to building a DIY investment portfolio.

Our View

This article is an attempt to provide clarity to the question and help with ‘ideas’. We are Independent Financial Advisers. We would never work in a way to limit our clients’ investment solutions provided from a restricted investment process; such a process, we believe, results in pushing “square pegs into round holes” in our view! We firmly believe in being able to select investment products and assets from the investment universe, rather than a ‘walled garden’ of funds and products, often limited to the ownership of the Restricted Advice Distributor.

Building an investment portfolio requires skills, experience, knowledge and discipline… We have yet to see an investor produce a ‘professional quality’ risk adjusted (suitable) investment portfolio, aligned to their specific needs, let alone rebalance the said portfolio and review it regularly. (The review process is as essential as the set up process, as personal circumstances and objectives change over time, along with economic outcomes).

Annual reviews are essential, where a conclusion of an ‘annual suitability review’ is concluded. This process assists investors to focus on their plans for the coming year, planning for change, if required.

Advised or Non Advised – Decisions?

We respect that investors should have the freedom to select if they require ‘financial advice’ services… which clearly we endorse, or buy products without receiving regulated advice. Some investors will want to DIY, which is why we make products available to investors, where we can, via our website so they can actually DIY – although this process provides no regulatory financial advice protection. Check out our website #BestPrice FS Investment page – https://www.bestpricefs.co.uk/investments/

We firmly believe that the consumer should have freedom of choice while fully understanding the ‘value add’ of expert advice – and what it can and can’t do.

Many investment products require ‘advice’ – as directed by the plan manager/manufacturer. As a regulated business, we do not decide whether a product requires ‘advice’ or not, we simply comply with providers’ instructions and the regulatory process. The

“complexity” of an investment is often the key identifier of the distribution method, as directed by the manufacturer. If a plan can be purchased without advice – experience and understanding of the risks is critical. We gather confirmation of this position via an Appropriate Assessment Questionnaire.

The recent Retail Distribution Review and the Financial Advice Market Review published on 1 May 2019 identified a need for balance in relation to investment distribution. The FCA stated “while regulator costs can be seen as the cost of doing business well, we are also aware that our actions can have a negative impact on the market and, by extension, on consumers”. Attached is a copy of the communication that we sent to a number of perceived leading financial journalists (no names stated) but, as expected, we have received no responses to date! More on this another time……..

Click the link to read the communication and more about what the FCA are looking at….

Please note that the products detailed in this article are by way of example and not to be seen as a recommendation to invest in the products. “Advice! requires a “suitability recommendation” in respect of how a product or combination of products produce a “suitable product suite” to meet an investor’s needs in relation to their specific circumstances, goals, aims, capacity for loss (and overall Risk Tolerance/Objective).

Our Recommendation

Our recommendation is to take advice at outset so an accurate picture of the investor’s position, goals, time horizon and capacity for capital loss can be clearly understood. Regular reviews are also imperative, as the discipline of reviews is where we see many failings as we see an investor’s portfolio suffer investment drift, not aligning to their changing circumstances through the passage of time! Investments also need reviewing, as identified with the recent high profile LF Woodford Equity Income Fund debacle.

Investment Process

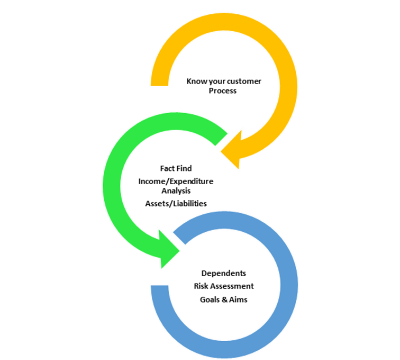

Providing Regulated Financial Advice requires a regulatory ‘Compliance process’ to be followed, which means that in order for an adviser to provide ‘advice’ to an investor a ‘Know Your Customer’ process/journey must be followed so that a recommendation is consistently applied, following a regulatory structure, in order to produce ‘suitable recommendations’ to meet the needs of consumers/investors. This is time consuming but time importantly spent.

The process of gathering the ‘KYC’ details involves the gathering of facts, such as income/expenditure, debt, asset values (including Pension), dependents, goals & aims and capacity for loss (generally via a comprehensive risk profiling tool), along with ‘soft facts’ involving personal details, history, knowledge and a client’s motivations. This process enables a product portfolio to be constructed having carried out ‘due diligence’ in relation to an investor and the products/plans that are recommended as suitable investment solutions, ensuring that a wide spread of asset classes, products and funds are purchased over geographies and sectors.

Click the link to read about ‘Our Approach’ –

Financial Planning

Building a financial plan requires consideration of the ‘full picture’ of a person or entities’ financial position, including protection needs. This article focuses on building an investment programme, attached is a link to a previously written article published on Friday 11 January 2019 by clicking on the following link: ‘Take control of your finances’ –

https://www.bestpricefs.co.uk/blog/take-control-of-your-finances-review-your-investment-pensions-and-insurance-positions/

Portfolio Construction

How do you require your investment assets to be constructed?

We select and monitor, with reviews, how to include the ‘Best of Breed’ investment funds and products from the investment universe – on an independent financial advice basis, considering risk objectives – in line with a long term realistic expectation of results.

The assumption is made in this article that an investor holds sufficient ‘contingency cash’ to avoid destruction of an investment plan recommended should cash be required which wasn’t foreseen at outset. The amount to be held in cash ‘instant access’ accounts should generally be at least 6 months of expenditure, but we recommend 12 months. (Note – the initial establishment cost of an advice plan is greater in year 1 – due to advice set up and establishment charges so early surrender is not an advisable course of action for investors!) Investments must always be seen to be longer term in nature so to regather set up costs and in order to ‘ride out’ the inevitable rollercoaster of volatility along the investment road …. Our view and recommendation to clients is that the minimum term for investing in ‘long only’ mutual type funds is 5 years. Structured Products and Deposits have contract terms which must be adhered to.

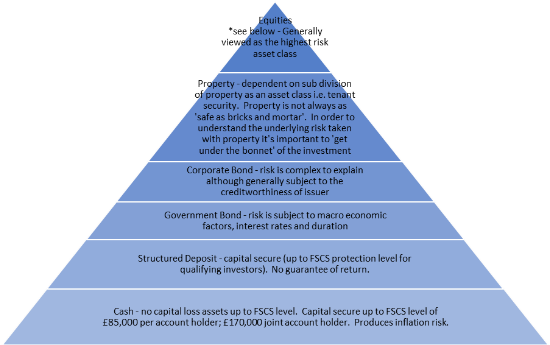

Risk Design – Asset Allocation

The general principle of investment risk can be easily explained in the visual (pyramid) below. As a business we get ‘under the bonnet’ of an investment and explain in detail how we construct an investment model, looking at past investment events in relation to volatility drawdown. Cue; past performance is not a guide to future performance. (As always, a regulatory statement in relation to the performance of an investment solution must be made!) Investment carries ‘Risk’ – therefore, in order to deliver suitable outcomes for clients and investors we work hard to make sure our clients receive advice that is clear, straightforward and ‘suitable’.

We must all prepare for the unexpected when it comes to investing. The recent Woodford Asset Management crisis identifies that results are certainly not guaranteed, even from one of the biggest brand names. Over exposure to a sector via a fund that has historically delivered superior returns can create damage. (Thankfully, we held limited exposure to Woodford’s Equity Income Fund – 2% or less in Risk Model 5, our medium risk investment portfolio). We used Woodford’s Equity Income Fund as further non-correlation to funds within the sector, as we had believed that at a point in time – like a faulty clock – Neil Woodford’s calls would deliver a change of results. Neil Woodford’s timing has now developed into requiring ‘reconstruction’, rather than a ‘major service’ which has, no doubt, created brand damage. We are therefore extremely pleased that we have remained focused on diversity, even within sectors and would not hold more than 10% in any ‘one’ fund in a portfolio.

(Nevertheless, the investment profession was not aware of investment ‘breaches’ by Woodford until recent developments – which is another good reason to ‘spread’ within an asset sector!)

Another famous Warren Buffet quote which is relevant to asset construction

– one to remember!

Investment Risk Scale

We use a scale that investors should be able to follow, in a simple way – 1 to 10. 1 being lowest capital risk and with lowest volatility, 10 being highest capital risk and highest level of prospective volatility.

Most ‘investors’, having completed a ‘Risk Profiler’ assessment, are generally between 4 – 6 on the risk scale, when considering the duration of the investment, tolerance to loss, goals and risk capacity to suffer loss.

An example: Risk increases from 1 – 10

Risk 1 – being cash like assets only (low in respect of volatility) – in our view this is for ‘saving’ and deposit based holdings. Investment develops where ‘Risk’ is taken, so our model 2 would hold 20% risk assets; 3 – around 30% risk assets; 4 – around 40% risk assets and so on, as a guide.

Risk 5 – being medium risk – is where the majority of investors see themselves in respect of risk capacity and tolerance. In reality, this is the risk area where most investors are placed for the medium to longer term (i.e. minimum 5 years investment time frame).

Risk 9 – being 90% equity (risk assets)

Risk 10 – being 100% risk assets, such as a FTSE 100 tracker fund – no diversity with other asset classes, Risk assets only. Often this would be a pure equity product, such as FTSE 100 tracker/ETF product.

We use a consistent process of fund selection, although of course varying the risk asset percentage which in turn increases the volatility as the scale increases.

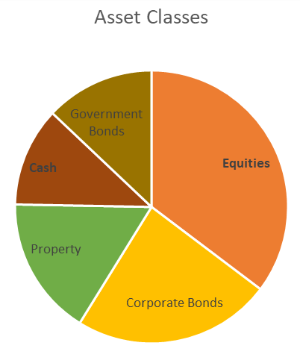

The general principle (in order to make retail investors aware of risk exposure) is that an investment risk model 5, on a scale of 1 to 10, may hold around 50% in equities, with the balance split between other asset classes of Government Bonds, Corporate Bonds, Property alternatives and Cash, thus producing a volatility outlook, both historically and prospectively. (The forward looking view is the imperative consideration).

Investors should note that there have been times where all asset classes (other than cash) have fallen heavily in unison. The global financial crisis produced such an investment experience! – Many investment grade Corporate Bonds behaved in a similar way to that of Equities, as many Debt assets were correlated.

Systematic Risk is the major concern to asset allocations, this is where investment risk becomes ‘undiversifiable’. Take a look at Systematic Risk on Investopedia – https://www.investopedia.com/terms/s/systematicrisk.asp

Political and economic news flow drives markets, often ignoring the ‘fundamentals’ of the investment picture. This is why the ‘sentiment’ of the market is often seen as driving the markets to be ‘Risk on’ or ‘Risk off’. A short term approach to investing is unwise, rarely producing suitable long term outcomes but, of course, experienced investors like to make ‘calls’ on asset prices…. No one has a crystal ball so a focusing on ‘one’s needs’ in relation to Risk/Return is imperative.

A study carried out by Morningstar in relation to behavioural finance is a useful read for investors. Click the link to read the article and the study – “Investing is simple, but not easy” – Warren Buffet

https://www.bestpricefs.co.uk/blog/behavioural-science-applied-to-investing-simple-but-not-easy/

A General Overview

Diversification

Holding a diversified (wide asset spread) portfolio in line with your personal risk tolerance and capacity for capital loss in order to meet your objectives produces the best investor outcomes in an uncertain world.

* Equities are often distinguished as having a division of risk within the asset class. In order to explain this in a simple way, a large multi-national (consumer staple company) would be expected to be more defensive than a small cap company. A company where products are purchased or consumed and ‘needed’ regardless of the economic position or outlook are generally viewed as less volatile than a company where the revenue (and share price) is influenced by unpredictable news-flow, economic factors or trends. Similarly investment funds provide a ‘Risk Objective’ – breaking down the assets/sectors and performance delivered – normally against a relative benchmark, so the investor can gather an understanding of ‘risk’ of the fund. (This being said, past performance is not a guide to future performance!).

I append below links to previous articles published for your information. These articles are available on the Best Price FS Blog and certainly worthy of a read and will assist with a wider, general understanding of ‘how to construct a quality financial plan’. It’s best the articles are read as a collective:

https://www.bestpricefs.co.uk/blog/an-investment-programme-for-the-long-term/ – This article provides details of ‘considerations’ when building an investment plan for the long term.

A further 3 articles help to explain and provide educational information to retail investors. Click the links below to read and follow information:

https://www.bestpricefs.co.uk/blog/investment-market-volatility/ – Investment Market Volatility Increases

https://www.bestpricefs.co.uk/blog/investing-is-a-marathon-journey-not-a-sprint/ – Investing is a Marathon Journey not a sprint ….

https://www.bestpricefs.co.uk/blog/political-and-economic-risks-and-portfolio-results/ – Political and Economic Risks and Portfolio Results

Structured Deposits

A Structured Deposit is generally invested in a ‘Contract’ that offers the potential to provide a return – linked to the performance of an index – that is mostly equity focused. The capital is secure up to the FSCS level (£85,000) (if qualifying) but the return is defined by the ‘contract terms’ at outset. Take a look at the range of Deposit Plans issued across the UK market – https://www.bestpricefs.co.uk/structured-products/.

Our transaction costs are priced at one of the lowest, if not the lowest based upon ‘value and service’ across the UK.

We produced an article which explains how Structured Deposits work, identifying a quality product. Click the link to read more – https://www.bestpricefs.co.uk/blog/investec-structured-deposits/

Structured Investments

Structured Investment Products are capital at risk products – again defined by the terms set with ‘contract’ at the outset (strike point). Often investment markets can fall or move laterally while still producing quality returns. Important considerations for investors in respect of selecting a suitable Structured Product are:

1. The strength of the issuer/counterparty

2. Barrier level

3. Contract Risk (overall)

4. Concentration Risk

The general rule is to limit exposure to one counterparty to no more than 10% of an investor’s capital, with no more than 20% exposed to Structured Capital at Risk products.

Inclusion of Structured Deposit and Investment Plans

Click the link to read why the inclusion of using ‘contract based’ Structured Investment products in portfolios – https://www.bestpricefs.co.uk/blog/including-structured-products-in-portfolios/

All investment plans/products should be viewed as medium to long term investments, although some contract terms are shorter than others, with terms running from 3 years to 10 years commonly.

The advice (regulatory) process requires a professional adviser to consider many factors, such as investment duration and, of course, the risk v return profile of investors, including capacity for loss. The assessment of the underlying investment (normally an index), along with the Counterparty (issuer – Banking or insurance companies) financial strength is also a major issue of assessment when providing advice.

Structures can take a ‘published shape’ which is focused for distribution to the general retail investor. These are Retail Investment Plans. Private Placements, which can be constructed in a bespoke way, are generally the domain of the experienced riskier investor. The terms can be very attractive but not published in the same way as retail products. Generally £250,000 is required to construct a private placement.

We can provide advice in relation to Bespoke Private Placement Structured Products. Contact us to start a discussion if required.

Investment focus – Growth/Income or Both?

A quality investment solution will build in a considerable amount of flexibility as ‘life delivers the unexpected’…

‘A perfect storm’ in my view is where an investor requires a major change to the investment plan, such as requiring ‘without notice’ surrender of an already established portfolio when investment markets are falling. What is often described as a ‘perfect storm’ with investment markets is where many investment factors, such as political and economic news flow and data conspire to produce negative sentiment, with no counter balance to ‘defend’ investment markets becoming over sold! This happens from time to time – driven by the human nature of Fear and Greed. A “sell off” transpires …..

The consideration of a Growth or Income portfolio, or combination of both, must consider ‘Perfect Storms’ as Capital and Income is sometimes required by investors unexpectedly! We make contact with our clients regularly (mostly weekly) in order to reinforce the need to identify and plan for change events… Advisers can’t plan what they are unaware of! Communication and forward planning is key to delivering best outcomes.

We often meet investors who describe themselves as ‘lower to medium risk’ investors, who are fully invested into Equities, either via Passive/Tracker products linked to main market indices and Structured Capital at Risk products. Often products purchased decades ago – held in Zombie funds which turn out to be completely unsuitable to an investor’s current needs. DIY investors rarely produce suitable outcomes for themselves. It must be noted that DIY investors do not benefit from the protection of the regulatory advice process so the Financial Ombudsman Service (FOS) will not be able to review a process where no advice has been provided. Only when the unforeseen happens, when investment failures develop, leading to a damaging outcome, do investors truly value quality advice, or indeed the regulatory protection required of advice.

We once met an investor who had described a defensive cash position as holding 40% in peer to peer lending! A very smart person but dangerous to themselves in respect of investment risk!

A forward thinking ‘Cashflow Plan’

Building a ‘cashflow plan’ certainly helps investors engage with longer term budgeting and with the investment process. If the process delivers too much complexity it can be disengaging to consumers, in our experience ……. Keep it simple to follow is best!

There are many progressive developments in the financial technology (Fintech) space. Cashflow modelling tools are certainly an increasing part of building a financial plan, taking a number of data points, combining risk and growth assumptions, producing a model – or a ‘track to run on’, as we prefer to call it, as investment returns are never certain.

Growth Focus

Where an investor is investing for growth, normally pre-retirement, using products and assets that are focused on growth is simple. An example of this would be a 45 year old investment for Retirement in a Pension Plan, expected to retire age 65 – a 20 year plan. (There are a number of variables that need consideration at various points, such as Pension Freedom at age 55 – although an annual review should essentially provide an update to the adviser so the investment assets can be altered, should the investment path change!)

Income Focus

Where an investment is required for income, normally at or in retirement, an income focus in relation to products should be considered and used. Income units, rather than accumulation units, held within funds (where available), as natural income can be distributed. Using income focused products such as Structured Deposit and Investment income funds – in line with the concentration risk already discussed, a portfolio that aims to deliver to our investors’ needs can be constructed, while being careful in relation to the many risks suffered when investing..

Where an investor has little or no ability to generate ‘new income or capital’ (generally in retirement) they often become naturally more defensive, so it’s again imperative to regularly consider an investor’s overall holdings.

Sequencing Risk

Investors are becoming increasingly aware of the risks associated with investment market movements (volatility) and the impact suffered by portfolios at a time when access to income and/or capital is required.

Investment markets produce volatility – fact. 2018 saw the UK’s main FTSE 100 index fall from broadly 7900 at its highest (mid 2018) to 6600 at the end of the year. Trade disputes between the US and China being the major concern, as 40% of the Globe’s trade is carried out by the two countries. The political and geo political environment creates concern most days of the year currently, driving volatility due to sentiment reactions.

The construction of an Income focused portfolio must consider the impact of severe investment volatility so the combination of the assets within the investment portfolio are placed into a position of danger when investment markets tumble. The ‘sequence’ in which the returns are generated in order to provide the income therefore becomes an imperative point so that ‘pound cost ravaging’ does not occur. Building a predictable, secure income over a variety of time horizons – leading to the long term delivery of an investor’s objective is the best plan in our view:

1 – 3 years

3 – 5 years

5 – 7 years

7 years plus…..

Financial jargon is becoming clear to regular retail investors and increasingly understood to a greater extent as advisers are better equipped to explain what the terms mean in ‘plain language’. Take a look at an article produced by Brooks Macdonald – Our Decumulation Strategy – An introduction to Sequencing Risk – https://www.brooksmacdonald.com/~/media/Files/B/Brooks-Macdonald-V4/documents/decumulation/Iintroduction-to-Sequencing-Risk.pdf?utm_source=Brooks%20Macdonald%20Asset%20Management&utm_medium=email&utm_campaign=10576005_220519-%20CoNews-%20Decumulation%202%20Sequencing%20Risk-%20SC&dm_i=9TF,6AOHX,ME5FCM,OUV02,1

Further Risks

Currency movements can create a significant impact to an individual’s financial position. Many of our clients hold overseas assets – property is a simple example of this.

Brexit, along with a strong dollar has impacted investors buying assets – often property overseas as sterling is weak, driven by uncertain political and economic factors. Import/Export businesses plan for currency movements, although many have become damaged since Brexit depending how payment is made, i.e. sterling or other global currencies.

(Don’t forget our F/X Money Transfer Service should you require the movement of one currency to another – at the Best Price! – https://www.bestpricefs.co.uk/app/foreign-exchange/

https://www.bestpricefs.co.uk/blog/may-3rd-market-updates/

https://www.bestpricefs.co.uk/blog/our-new-foreign-exchange-money-transfer-service/

Growth and Income

Investors generally have an objective for growth and income where an investor requires growth for a further 5 or 10 years, while providing a ‘top up’ to their income from capital previously invested; often to support a reduced income, until a retirement product (Pension) commences. Of course, a mix of all asset classes is used in this position, with a focus on the essential requirement of the income provision.

Investment Solutions – long only funds or mutual funds

Our view is that investors and professional investment recommendations in respect of a ‘suitable’ investment strategy must remain mindful of investment spread and diversity.

What is meant in this regard is that a suitable investment portfolio should not hold more than 10% in a single fund in an asset sector and consider stock duplication. So to explain with clarity, if 15% was to be allocated to UK Equities, no more than 10% should be held in respect of an investor’s asset in a single fund, in our view, preferably split between 5-6 leading funds based upon research and due diligence.

Similarly, in respect of Structured Investment products, a limit of 10% exposure to a specific counterparty/issuer should be held, with no more than 20% to Structured Capital at Risk Investment products. This is common sense in reality and reduces concentration risk should a product fail or seriously underperform, as has recently been experienced by Woodford Asset Management. A mixture of focused funds (often limited to around 40-50 stocks) combined with a mixture of other quality funds, holding a wider range of stocks within the fund, provide a good example of investment diversity – limiting stock over lap, where possible, meaning the same stocks are not duplicated within funds.

Growth Required

An example of a Growth focused portfolio – where an investor is medium risk in nature, i.e. 5/6 on a scale of 1-10 and investing for the long term.

The examples assume that contingency (emergency) capital is held outside of the specific investment plan, so no provision is required of cash management in these examples

Bedrock of Investment Plan

Growth Portfolio – medium risk investors – long term focus (10 years plus)

1. We like the Investec FTSE 100 3 Year Deposit Plan 50. Suggested hold 5% of investable capital. This plan provides contract terms which offer the potential to provide 5% simple interest if the FTSE 100 is one point higher than the strike point after 3 years. There is no capital at risk and the plan is protected up to the FSCS level £85,000 for eligible investors. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/ftse-100-3year-deposit-plan/

2. Investec FTSE 100 Kick Out Deposit Plan 86. Suggested hold 5% of investable capital. Again, a capital secure plan, up to the FSCS protection level. The plan provides the potential to provide 6% p.a. simple interest from a 3 year review point. Reviews are after 3, 4 and 5 years should the FTSE 100 not increase. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/ftse-100-kick-out-deposit-plan/

3. Investec FTSE 100 6 Year Deposit Plan 12. Suggested hold 5% of investable capital. Again, the return of capital deposit with FSCS protection for eligible investors should Investec destruct! Provides the potential for 42% return, if the FTSE 100 is higher than 100% of its starting level after 6 years (paid at maturity). This is equivalent to 7% p.a. (not compounded). Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/ftse-100-6year-deposit-plan/

4. iDAD Callable Deposit Plan Issue 4 (July 2019). Suggested hold 5% of investable capital. This is a seven year, 2 week Deposit Plan based upon the performance of the FTSE 100 index. the deposit plan is constructed to offer the potential to return 7% p.a. to the redemption date, if the deposit taker calls the investment early or 2% participation in any growth in the FTSE 100 index at maturity. Capital secure, protected up to £85,000 via FSCS for eligible investors. Counterparty – Goldman Sachs. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/callable-deposit-plan/

5. Tempo Long Growth Accelerator Plan. Suggested hold 5% of investable capital. Option 2 – this is a 10 year investment plan providing the potential to ‘kick out’ a return of 105% at year 5, which is equivalent to 20.5% p.a. simple of 15.16% compounded, with the maximum return at year 10 is equivalent to 18% p.a. or 10.84% p.a. compound. Counterparty – Société Générale. Barrier level 60%. Counterparty Société Générale. Barrier Level 60%.

Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/long-growth-accelerator-plan-option2/

6. Tempo Long Kick Out Plan. Suggested hold 5% of investable capital. Option 1 provides the potential to provide 8.25% p.a. which is payable if the relevant index is at or above 90% of the start level on any ‘kick out’ anniversary from year 3 onwards. Counterparty Société Générale. Barrier level 60%.

See the article – Tempo’s latest product suite – 1 May 2019

7. Meteor FTSE STOXX Defensive Kick Out Plan. Suggested hold 5% of investable capital. This plan has a maximum 7 year 3 week duration offering the potential to deliver 10% p.a. gross return provided the FTSE and Euro Stoxx are at or above a reducing reference point. Counterparty HSBC Bank plc. Barrier level 60%.

Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/meteor-ftse-stoxx-defensive-kick-out-plan/

8. Mariana 10:10 Plan – July 2019 (Option 2) Suggested hold 5% of investable capital. A maximum 10 years and two week structured product that offers the potential for maturity at the end of year 2, with a return of 10.30% p.a. with a return of 10.30% p.a. per year, provided the FTSE 100 is at or above 100% the start level on one of the kick out dates.

Counterparty – Citigroup Global Markets Ltd

Barrier level 70%

Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/10-10-ftse-kick-out-plan2/

Long Only Investment Portfolio – Balance invested in a range of leading funds (generally 50) spread across asset classes

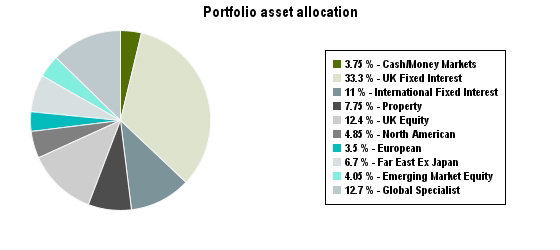

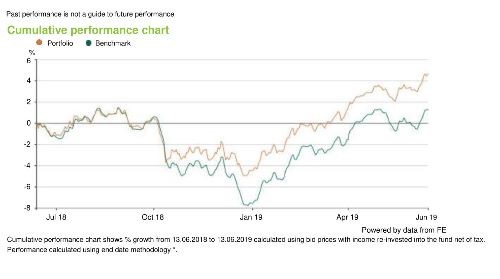

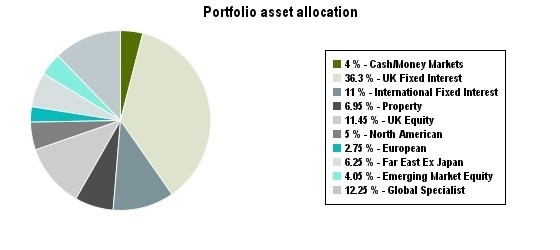

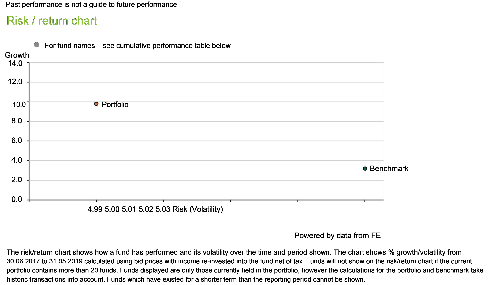

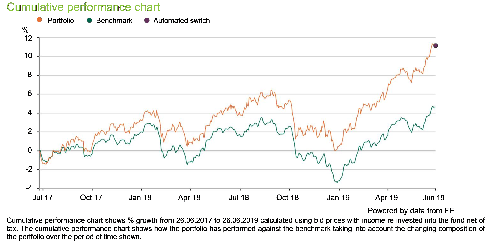

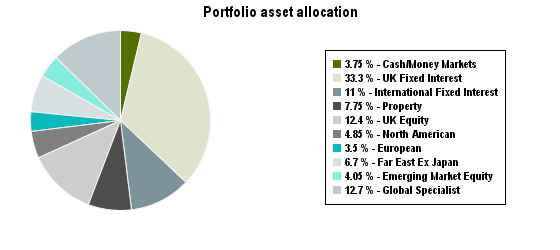

9. We have constructed a risk adjusted investment portfolio using quality funds which have delivered relative benchmark and peer beating results, relative to risk, with a long term track records.

An example of the asset allocation is detailed below:

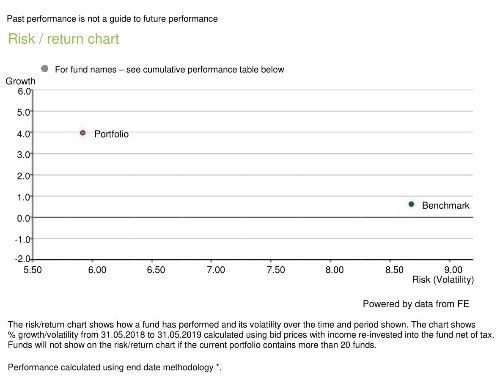

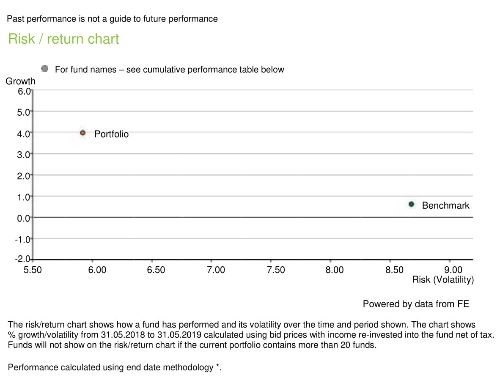

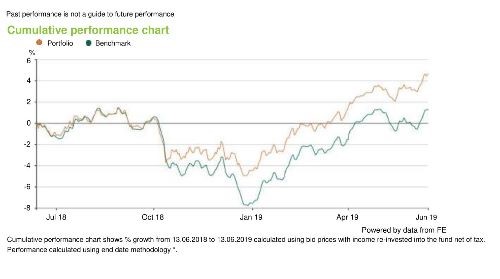

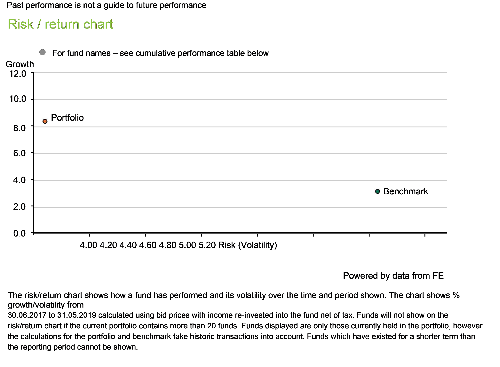

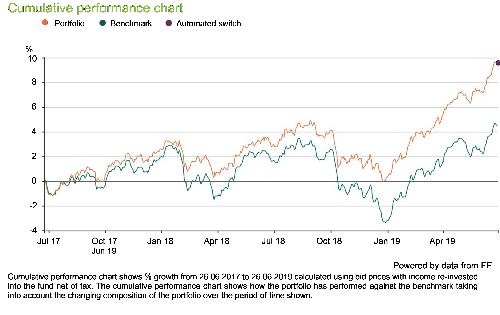

Asset Allocation for Risk Model 5 performance and volatility results.

Volatility

Cumulative Performance

We must state Past Performance is not a guide to future performance. As previously stated ‘ongoing reviews’ of such a portfolio is essential so the solution remains on track with an investor’s needs.

Growth and Income Required Investments

1. We like the Investec FTSE 100 3 Year Deposit Plan 50 Suggested hold 5% of investable capital. This plan provides contract terms which offer the potential to provide 5% simple interest if the FTSE 100 is one point higher than the strike point after 3 years. There is no capital at risk and the plan is protected up to the FSCS level £85,000 for eligible investors. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/ftse-100-3year-deposit-plan/

2. Investec FTSE 100 Kick Out Deposit Plan 86. Suggested hold 5% of investable capital. Again, a capital secure plan, up to the FSCS protection level. The plan provides the potential to provide 6% p.a. simple interest from a 3 year review point. Reviews are after 3, 4 and 5 years should the FTSE 100 not increase. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/ftse-100-kick-out-deposit-plan/

3. Investec FTSE 100 Income Deposit Plan 28 – monthly. Suggested hold 5% of investable capital. Investment Term 6 years. A Deposit based plan based upon the performance of the FTSE 100 Index. The plan provides the potential to provide an income payment of 3.12% p.a. paying 0.26% per month if the FTSE 100 is higher than 75% and its starting level on each monthly anniversary date (equal to 3.12% p.a.).

https://www.bestpricefs.co.uk/structured-products/ftse-100-income-deposit-plan-monthly/

4. Investec Defensive Income Plan 17 – Option 2. Suggested hold 5% of investable capital. A defensive Income Plan that aims to provide 1.675% per quarter income 6.7% p.a. Investment term 8 years. The product is capital at risk with a barrier level of 60%. Counterparty is Investec Bank.

https://www.bestpricefs.co.uk/structured-products/ftse-100-defensive-income-plan-option2/

5. iDAD Callable Deposit Plan Issue 4 (July 2019). Suggested hold 5% of investable capital. This is a seven year, 2 week Deposit Plan based upon the performance of the FTSE 100 index. the deposit plan is constructed to offer the potential to return 7% p.a. to the redemption date, if the deposit taker calls the investment early or 2% participation in any growth in the FTSE 100 index at maturity. Capital secure, protected up to £85,000 via FSCS for eligible investors. Counterparty – Goldman Sachs. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/callable-deposit-plan/

6. Tempo Long Growth Accelerator Plan. Suggested hold 5% of investable capital. Option 2 – this is a 10 year investment plan providing the potential to ‘kick out’ a return of 105% at year 5, which is equivalent to 20.5% p.a. simple of 15.16% compounded, with the maximum return at year 10 is equivalent to 18% p.a. or 10.84% p.a. compound. Counterparty – Société Générale. Barrier level 60%. Counterparty Société Générale. Barrier Level 60%.

Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/long-growth-accelerator-plan-option2/

7. Tempo Long Kick Out Plan. Suggested hold 5% of investable capital. Option 1 provides the potential to provide 8.25% p.a. which is payable if the relevant index is at or above 90% of the start level on any ‘kick out’ anniversary from year 3 onwards. Counterparty Société Générale. Barrier level 60%.

See the article – Tempo’s latest product suite – 1 May 2019

8. Mariana FTSE Defensive Income Kick Out Plan – July 2019. Suggested hold 5% of investable capital. A maximum 10 year 2 week investment offering a potential return of 1.575% per quarter, providing the closing price of the index is at or above 75% of the start level on each observation date. Counterparty is Morgan Stanley. Barrier level is 65%.

https://www.bestpricefs.co.uk/structured-products/ftse-defensive-income-kick-out-plan/

9. Long only investment portfolio – balance invested in a range of leading funds (generally 50) spread across asset classes

We have constructed a ‘long only’ risk adjusted investment portfolio using quality funds which have delivered relative to benchmark and peer beating results, relative to risk, with a long term track record.

An example of the asset allocation is detailed below. We would use a blend of income and accumulation fund options in order to deliver the required focus of Growth with Income. An example of the investment split could be:

Growth and Income – long only funds Portfolio

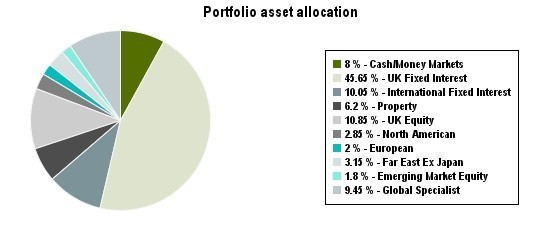

Using 20% of the investable capital in Risk Model 4

Asset Allocation for Risk Model 4 with performance and volatility results.

Volatility

Cumulative Performance

Past performance is not a guide to future performance

Using 40% of the investable capital in Risk Model 5

Asset Allocation for Risk Model 5 with performance and volatility results.

Volatility

Cumulative Performance

Past performance is not a guide to future performance

Income Portfolio

1. We like the Investec FTSE 100 3 Year Deposit Plan 50 Suggested hold 5% of investable capital. This plan provides contract terms which offer the potential to provide 5% simple interest if the FTSE 100 is one point higher than the strike point after 3 years. There is no capital at risk and the plan is protected up to the FSCS level £85,000 for eligible investors. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/ftse-100-3year-deposit-plan/

https://www.bestpricefs.co.uk/structured-products/ftse-100-kick-out-deposit-plan/

3. Investec FTSE 100 Income Deposit Plan 28 – monthly. Suggested hold 5% of investable capital. Investment Term 6 years. A Deposit based plan based upon the performance of the FTSE 100 Index. The plan provides the potential to provide an income payment of 3.12% p.a. paying 0.26% per month if the FTSE 100 is higher than 75% and its starting level on each monthly anniversary date (equal to 3.12% p.a.).

4. Investec Defensive Income Plan 17 – Option 2. Suggested hold 7% of investable capital. A defensive Income Plan that aims to provide 1.675% per quarter income 6.7% p.a. Investment term 8 years. The product is capital at risk with a barrier level of 60%. Counterparty is Investec Bank.

https://www.bestpricefs.co.uk/structured-products/ftse-100-defensive-income-plan-option2/

5. iDAD Callable Deposit Plan Issue 4 (July 2019). Suggested hold 5% of investable capital. This is a seven year, 2 week Deposit Plan based upon the performance of the FTSE 100 index. the deposit plan is constructed to offer the potential to return 7% p.a. to the redemption date, if the deposit taker calls the investment early or 2% participation in any growth in the FTSE 100 index at maturity. Capital secure, protected up to £85,000 via FSCS for eligible investors. Counterparty – Goldman Sachs. Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/callable-deposit-plan/

6. Tempo Long Growth Accelerator Plan. Suggested hold 5% of investable capital. Option 2 – this is a 10 year investment plan providing the potential to ‘kick out’ a return of 105% at year 5, which is equivalent to 20.5% p.a. simple of 15.16% compounded, with the maximum return at year 10 is equivalent to 18% p.a. or 10.84% p.a. compound. Counterparty – Société Générale. Barrier level 60%. Counterparty Société Générale. Barrier Level 60%.

Click the link to read about the product terms:

https://www.bestpricefs.co.uk/structured-products/long-growth-accelerator-plan-option2/

7. Tempo Long Kick Out Plan. Suggested hold 5% of investable capital. Option 1 provides the potential to provide 8.25% p.a. which is payable if the relevant index is at or above 90% of the start level on any ‘kick out’ anniversary from year 3 onwards. Counterparty Société Générale. Barrier level 60%.

See the article – Tempo’s latest product suite – 1 May 2019

8. Mariana FTSE Defensive Income Plan – July 2019. Suggested hold 5% of investable capital. A maximum 10 year 2 week investment offering a potential return of 1.575% per quarter, providing the closing price of the index is at or above 75% of the start level on each observation date. Counterparty is Morgan Stanley. Barrier level is 65%.

https://www.bestpricefs.co.uk/structured-products/ftse-defensive-income-kick-out-plan/

Income Long Only Investment Portfolio – Balance invested in a range of leading funds (generally 50) spread across asset classes

As the focus is to provide income the balance of the investment programme is focus on the sequence of risk, so a medium risk investor could consider the shorter term view as 1-3 years as holding 20% of investable capital with the balance of 40% held for longer term income and growth potential – drawing ‘income’ from deposit – cash like funds.

The investment risk would consider the individual needs of the investor, although an example would be to hold 20% in our Risk Model 3 with 40% held in Risk Model 5. Our risk model 3 asset allocation is currently as follows:

Asset Allocation for Risk Model 3 with performance and volatility results.

Volatility

Cumulative Performance

Past performance is not a guide to future performance

We must express that the discussion if including funds and products, identified in this article are examples of product solutions we like, although this is NOT a recommendation to invest. An advice recommendation must always be provided once the full holistic position of an investor’s position is fully understood, enabling a recommendation in respect of suitability to be made.

Sustainable/Ethical Investing

Investors are increasingly asking how they can invest sustainably. Sustainable investing is often called:

Ethical Investing, Green Investing or Socially Responsible investing

We can arrange a portfolio of investments that invest in a ‘sustainable’ way at low cost. Get in touch if you would like advice in this area.

The extremely topical and very important global coverage of climate change is driving investor considerations. the Task Force on climate related financial disclosures, TCFD, is becoming widely understood in relation to the recommendations for better climate related financial disclosures. Click the link to read more:

Tax Products – VCT/EIS/BPR Schemes

An individual’s financial position, especially in relation to the tax suffered, needs to be understood prior to advice being delivered.

The use of allowances is essential. Investors should use ISA, Pension and Capital Gains Tax Allowances as ‘wrappers’ for investments. This article is an attempt to illustrate the complexity and due diligence required when making investment decisions/investments. Investing is simple – but not easy!

At Best Price FS we focus on making access to products and advice (consultancy) services straightforward and affordable.

If you would like to gather Independent Financial Advice simply get in touch – we make the rest easy to follow.

Needless to say, Best Price FS, as Independent Financial Advisers, provide advice at low cost in relation to tax products.