Potential return 6% Structured Deposit rate launch

A new Structured Deposit FTSE 100 Kick-Out-Plan 78 has been launched today by Investec. The plan offers the potential for maturity – at the end of 3, 4, 5 and 6 years with a payment equal to 6% per annum (NOT COMPOUNDED) if the FTSE 100 is above the starting level/strike point of the plan, after 3, 4, 5 to the 6-year maturity. The potential kick-out dates are 30/07/21, 29/07/22 and 31/07/23.

Key Risk

If the FTSE 100 finishes equal to or lower than it’s starting level, investors will only get back the initial deposit amount, with no return. The term of the product is 6 years but if the FTSE 100 is higher than the “starting point” after year 3, 4 or 5 a kick-out at the rate of 6% would occur. (It is important that it is understood that this communication is not to be seen as “advice”, as “advice” must be personal to a consumer’s needs and financial position). If you think a product such as this meets with your needs, simply get in touch so “advice” can be provided if required. Our price points for both advice transactions and non-advised transactions are amongst the most competitive available in the UK, so we are confident that if such a product fits your needs, you will benefit from the “best price” to purchase the plan.

How a Structured Deposit is constructed and set up

Structured deposits — These are essentially a fixed term deposit account, but instead of the interest being earned at a set or variable rate, returns are dependent upon the performance of the underlying asset, such as the FTSE 100 index.

Like a deposit account, these usually offer the same eligibility of recourse to Financial Services Compensation Scheme in the event of a counterparty default during the investment term. UK eligible claimants have a right to claim up to £85,000 per individual per institution in such circumstances.

While no investment is completely risk free, structured deposits are designed to return investors’ original capital as a minimum at maturity, regardless of market movements.

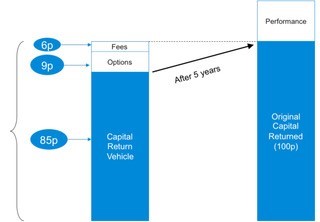

The diagram below shows in very simple terms how a Structured Deposit works in practice.

Consider a product that aims to return the initial deposit at maturity plus an interest payment linked to the performance of an underlying asset or index, i.e. the FTSE 100 index. For every 100p invested, 85p is used to return the initial deposit at maturity. This is because the provider is able to “lock in” a rate of interest over 5 years sufficient to return the initial deposit. 6p is used to build the product and cover expenses with the remaining 9p being used to buy financial instruments which provide the performance element (interest payment). The performance element could say, if the FTSE 100 is higher at maturity then a fixed interest payment of 35% will be made, however if the FTSE 100 finishes lower at maturity then only the initial deposit will be returned.

A typical Structured Deposit – 5-year plan linked to the FTSE100 Index

This Plan has been designed for investors who are looking for alternatives to fixed rate cash products, such as a fixed rate bond, in order to achieve capital growth over a 6-year term but are able to accommodate receiving their money back before the end of the 6-year term, should a kick out arise or locking the capital away for up to 6 years.

Investors are willing to take the risk that actual returns achieved may be lower than fixed rate cash products, but do not wish to risk losing their initial deposit and therefore this Plan is aimed at investors who have a medium-low appetite for risk. There is no guarantee of the 6% return. In order to benefit from the return, the FTSE 100 must be higher than the starting point after 3, 4, 5 years to maturity.

Investors will understand that the potential returns of this Plan are linked to the performance of the FTSE 100, and that the Plan can mature early. (Past performance of the investment markets is not a guide to future performance)

An example of a current Structured Deposit is the FTSE 100 Kick-Out Deposit plan

Are there any compensation arrangements in place?

This deposit plan is eligible for Financial Services Compensation Scheme (FSCS) protection. The FSCS can pay compensation to depositors if a bank is unable to meet its obligations, for example if it fails or becomes insolvent. Most depositors, including most individuals and businesses, are covered by the scheme.

In respect of deposits, an eligible depositor is entitled to claim up to £85,000. For joint accounts each account holder is treated as having a claim in respect of their share so, for a joint account held by two eligible depositors, the maximum amount that could be claimed would be £85,000 each (making a total of £170,000). The £85,000 limit relates to the combined amount in all the eligible

If you have any questions about this product, simply get in touch.

A number of new Plans are being launched on our website, so take a look at the Structured Products and Deposits, to see if any attract you. (Check out our blog for regular product and financial updates)

Click to view our latest structured deposit plans.